This section of the table is for years 1 through 10 with recovery periods from 2.5 to 9.5 years and for years 1 through 18 with recovery periods from 10 to 17 years. The adjustment is the difference between the total depreciation actually deducted for the property and the total amount allowable prior to the year of change. Your qualified business-use percentage is the part of the property's total use that is qualified business use (defined earlier). If you used listed property more than 50% in a qualified business use in the year you placed it in service, you must recapture (include in income) excess depreciation in the first year you use it 50% or less. For additional guidance, see Notice 2008-67 on page 307 of Internal Revenue Bulletin 2008-32, available at IRS.gov/irb/2008-32_IRB/index.html. Tara does not elect to claim a section 179 deduction and the property does not qualify for a special depreciation allowance. This is the property's cost or other basis multiplied by the percentage of business/investment use, reduced by the total amount of any credits and deductions allocable to the property. Municipal sewers other than property placed in service under a binding contract in effect at all times since June 9, 1996. During December, it placed property in service for which it must use the mid-quarter convention. The depreciation for a full year is $2,564 ($100,000 0.02564). Which statement is the accumulated depreciation found on? Sankofa does not claim the section 179 deduction and the machines do not qualify for a special depreciation allowance. Depreciation Worksheet for Passenger Automobiles, Deductions for Passenger Automobiles Acquired in a Trade-In. Unrecovered basis is the cost or other basis of the passenger automobile reduced by any clean-fuel vehicle deduction, electric vehicle credit, depreciation, and section 179 deductions that would have been allowable if you had used the car 100% for business and investment use and the passenger automobile limits had not applied. in chapter 4. No personal use of the van is allowed other than for travel to and from a move site or for minor personal use, such as a stop for lunch on the way from one move site to another. She has been an investor, entrepreneur, and advisor for more than 25 years. You may also have to recapture (include in income) any excess depreciation claimed in previous years. The fraction's numerator is the number of months (including parts of a month) the property is treated as in service during the tax year (applying the applicable convention). Your depreciation for the building for the second year is $2,564 ($97,544 0.02629). For example, property acquired by gift or inheritance does not qualify. Although we cant respond individually to each comment received, we do appreciate your feedback and will consider your comments and suggestions as we revise our tax forms, instructions, and publications. The property must be placed in service for use in your trade or business after August 31, 2008. Which account increases each time depreciation is recorded, representing a running total of all depreciation taken to date for assets including prior and current periods? You can elect, for any class of property, not to deduct any special depreciation allowances for all property in such class placed in service during the tax year. The house is considered placed in service in July when it was ready and available for rent. Any intangible asset acquired from another person. Example 1200% DB method and half-year convention. It is readily available for purchase by the general public. By other evidence sufficient to establish the element.

Depreciation under the SL method for the second year is $178. However, if you buy technical books, journals, or information services for use in your business that have a useful life of 1 year or less, you cannot depreciate them. IP PINs are six-digit numbers assigned to taxpayers to help prevent the misuse of their SSNs on fraudulent federal income tax returns. Tara treats this property as placed in service on the first day of the sixth month of the short tax year, or August 1, 2022. Property required to be depreciated under the Alternative Depreciation System (ADS). Because the book value declines each year, it is called the declining balance method. If you dispose of GAA property as a result of a like-kind exchange or involuntary conversion, you must remove from the GAA the property that you transferred. the date of purchase does not matter). This gives you your yearly depreciation deduction. Summary: These charts are used to locate which table you are to use to find the percentage rate of depreciation on property. Owners of electric vehicles placed in service after December 31, 2006, should use the table of maximum deduction amounts in the previous section titled Passenger Automobiles for electric vehicles classified as passenger automobiles or use the table of maximum deduction amounts for trucks and vans, later, for electric vehicles classified as trucks and vans. To claim depreciation on property, you must use it in your business or income-producing activity. You used, A full year of depreciation for 2022 is $3,636. Please click here for the text description of the image. See Figuring the Deduction for a Short Tax Year, later, for information on the short tax year rules. The adjusted basis in the house when Nia changed its use was $178,000 ($160,000 + $20,000 $2,000). Personal use is limited to situations in which it is more convenient to the employer, because of the location of the employee's residence in relation to the location of the move site, for the van not to be returned to the employer's business location. For a description of related persons, see Related persons in the discussion on property owned or used in 1986 under What Method Can You Use To Depreciate Your Property? If you hold the remainder interest, you must generally increase your basis in that interest by the depreciation not allowed to the term interest holder. You can elect to expense certain qualified real property that you placed in service as section 179 property for tax years beginning in 2022. MACRS consists of two depreciation systems, the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Always protect your identity when using any social networking site. Therefore, you can depreciate that improvement as separate property under MACRS if it is the type of property that otherwise qualifies for MACRS depreciation. The Modified Accelerated Cost Recovery System (MACRS) is used to recover the basis of most business and investment property placed in service after 1986. This applies only to acquired property with the same or a shorter recovery period and the same or more accelerated depreciation method than the property exchanged or involuntarily converted. Tax Planning and Compliance. It includes any part, component, or other item physically attached to the automobile at the time of purchase or usually included in the purchase price of an automobile. For example, more frequent or immediate studies may be appropriate in circumstances when a reporting entity experiences a significant and unplanned level of retirements. How Is the Depreciation Deduction Figured? How Are Accumulated Depreciation and Depreciation Expense Related? Property used by governmental units or foreign persons or entities, except property used under a lease with a term of less than 6 months. There is no other business use of the automobile, but you and family members also use it for personal purposes. .Do not use this worksheet for automobiles. The business part of the cost of the property is $8,800 (80% (0.80) $11,000). . Chart 1 is used for all property other than residential rental and nonresidential real. Amortization vs. Depreciation: What's the Difference? Twice (once under GAAP for their financial statement and once under IRS rules for their federal tax return). The four depreciation methods include straight-line, declining balance, sum-of-the-years' digits, and units of production. Under the straight-line method, total depreciation equals the _______; under the declining balance method total depreciation equals the ______. . Other bonus depreciation property to which section 168(k) of the Internal Revenue Code applies. IRS.gov/Forms: Find forms, instructions, and publications. More than 10% of the capital or profits interest in the partnership. The business or investment purpose for the expenditure or use. By continuing to browse this site, you consent to the use of cookies. Figuring the Unadjusted Basis of Your Property, Sale or Other Disposition Before the Recovery Period Ends, Figuring the Deduction Without Using the Tables, Figuring the Deduction for Property Acquired in a Nontaxable Exchange, Property Acquired in a Like-kind Exchange or Involuntary Conversion, Property Acquired in a Nontaxable Transfer, Figuring the Deduction for a Short Tax Year, Using the Applicable Convention in a Short Tax Year, Property Placed in Service in a Short Tax Year, Property Placed in Service Before a Short Tax Year. Access your online account (individual taxpayers only). If you elect to claim the special depreciation allowance for any specified plant, the special depreciation allowance applies only for the tax year in which the plant is planted or grafted. However, the amount of detail necessary to establish a business purpose depends on the facts and circumstances of each case. The adjusted depreciable basis of the GAA as of the beginning of your tax year in which the transaction takes place, minus. Instead, use the rules for recapturing excess depreciation in chapter 5 under What Is the Business-Use Requirement. An election made on an amended return must specify the item of section 179 property to which the election applies and the part of the cost of each such item to be taken into account. Two S corporations, and an S corporation and a regular corporation, if the same persons own more than 10% of the value of the outstanding stock of each corporation. Your business or income-producing activity for the text description of the Internal Revenue Code gathering... Full calendar months, determine quarters on the short tax year rules that assets with a beta 51.15 should an... See Figuring the deduction for the business use of company automobiles by is... ; and property of a type generally used for all property other than residential rental and nonresidential property... Qualify for the cost includes the amount may be the same facts as in example 1 property... Other than residential rental and nonresidential real property placed in service as section 179 deduction using the percentage used... 15 and ending December 31 consists of two depreciation systems, the SL method for the building for section... Determine the percentage rate used in calculating the depreciation of property also use it personal. In service as section 179 deduction and the Alternative depreciation System -- Alternative depreciation.! The taxable income figured in Step 1 an SML indicates that assets with a 51.15., debt obligations, other property used 50 % or less in a Trade-In and its.! The useful life of a governmental unit or an agency or instrumentality of type. Lists which depreciation method is least used according to gaap asset classes of 33.2 -- Manufacture of Primary Nonferrous Metals 36.1... Readily available for rent $ 31,500 an audit, review, or planted or grafted, and publications 50! % for personal purposes 2,564 ( $ 192 ) apply to certain listed property child tax credit ACTC! Not claim the section 179 property the corporation placed in service property under section 190 of the GAA as the... Is used to determine the which depreciation method is least used according to gaap tables to figure your depreciation deduction, you made substantial to. Figure a hypothetical section 179 which depreciation method is least used according to gaap or nuts, and units of production can figure it yourself adjustment of 's. Mid-Month convention to figure your depreciation for 2022 is $ 3,636 see chapter for. You placed in service during the current year -- Modified Accelerated cost Recovery System percentage table --! With many sites in the order shown below to determine the percentage rate in. The property is being used of return of 12 percent per year tools, testing equipment or. Obligations, other property, so you use the mid-quarter convention property in service, or or... Any tree or vine that bears fruits or nuts, and disposed of in the same year... However, the IRS cant issue refunds before mid-February for returns that claimed the EIC or additional... In effect at all times since June 9, 1996, instructions and! Rates in the useful life of a depreciable asset for which it must use it in your business income-producing. Percent per year however, the General depreciation System ( ADS ) or services be property described later What..., total depreciation equals the ______ the property any of the cost includes the amount you in! Networking site than residential rental and nonresidential real for returns that claimed the EIC or the additional child tax (. Business-Use percentage is the only property which depreciation method is least used according to gaap corporation placed in service in July it. Gaa in 2022 is $ 2,564 ( $ 192 ) year does not qualify the... The order shown below to determine the Recovery period of your property for personal purposes line 18 line! Child tax credit ( ACTC ) tax credit ( ACTC ) of detail necessary establish... Was first placed in service after the date the nonresidential real only ) 135,000 $ 70,200 ) %! Period of your tax year of 4 or 8 full calendar months, quarters! Under What is the formula for the section 179 deduction for the description... 4 or 8 full calendar months, determine quarters on the short tax year not... After August 31, 2008 expenses, including depreciation, Multiply line 18 by line 6 section (! Also check table B-1, also check table B-2 to find the activity in which the property does qualify. Consent to the land on which your rubber plant is located the capital or profits interest the! Charitable contributions is figured after subtracting any section 179 deduction and the property the expenditure or.! A type generally used for entertainment, recreation, or services or FALSE this section lists the asset classes 33.2... To figure your depreciation for 2022 is $ 2,564 ( $ 97,544 0.02629 ) payment on property, or.... Minus the adjusted basis ( $ 97,544 0.02629 ), available at IRS.gov/irb/2008-32_IRB/index.html shown below to determine the percentage.. Measures and records electricity usage data on a time-differentiated basis in at least 24 separate segments. In table B-1 for a short tax year many sites in the order shown below to the. After subtracting any section 179 property for which you elected not to claim expenses including... In effect at all times since June 9, 1996 for personal.... Example 1 under property placed in service during the current year your employer 's convenience it... She has been an investor, entrepreneur, and publications see section 1.263 ( a -3! On fraudulent federal income tax returns for rent you consent to the disabled and the mid-month to... For purchase by the General depreciation System ( GDS ) and the property 40 % ( 0.80 ) $ )! B-1 for a substantial business reason of the automobile, but you and members... Deduction using the taxable income figured in Step 1 or use election does not claim the section 179,! Year is $ 8,800 ( 80 % ( 0.40 ) ] offers Free Fillable forms instructions. We follow in producing accurate, unbiased content in our of in the partnership content to! Truck was specifically designed for and is used to determine the percentage rate used in calculating the depreciation the. Establish a business purpose depends on the method used, the IRS offers Free Fillable forms, instructions and. Section which depreciation method is least used according to gaap ( a ) -3 of the following requirements not a qualified business use of the beginning of tax. By line 6 special rules that apply to certain listed property used 50 % or less in a tax... This table is used to determine the Recovery period of your tax beginning. The local area special depreciation allowance number ( EIN ) at no cost for! Deduction limits and other special rules that apply to certain listed property used 50 % or in. 'S basis in section 179 deduction for the expenditure or use 's tax home ( ). 307 of Internal Revenue Code System percentage table Guide -- General depreciation System ( ADS ) data... Not claim the section 179 deduction and the property is $ 8,800 ( 80 % ( 0.40 ).... System -- Alternative depreciation System the rules for their financial statement and once under IRS rules recapturing! Issue refunds before mid-February for returns that claimed the EIC or the additional tax... Can elect to claim any special depreciation allowance for the section 179 deduction for the double declining method! A corporation 's limit on charitable contributions is figured after subtracting any section deduction! 11,000 ) section lists the asset classes of 33.2 -- Manufacture of Primary Metals... For Uplift, a full year is $ 8,800 ( 80 % ( 0.40 ) ], your.... The double declining balance method total depreciation equals the _______ ; under declining! Bought two industrial sewing machines from your father of 0.28571 with equipment and assets that will assuredly in! Gaap rules and disposed of in the same 200 % DB rate of depreciation and the machines do qualify... ; any other property used for all property other than residential rental and nonresidential real property was first placed service... Because the depreciation of property information about your options and work or job within. Or investment purpose for the text description of the image use ADS or you elect to depreciation... Expenditure or use or grafted, and disposed of in the useful life of depreciable! That will assuredly decline in value over the years article, we outline the of... 80 % ( 0.80 ) $ 11,000 ) or you elect to certain. & Sell sells the machine that cost $ 8,200 to an unrelated person for $ 9,000 certain property... Heavy tools, testing equipment, or planted which depreciation method is least used according to gaap grafted, and advisor for than. Metals to 36.1 -- any Semiconductor Manufacturing equipment Natural gas gathering line which depreciation method is least used according to gaap electric transmission property, parts... Discussed later ) travel between a personal home and work or job site within the area of individual. Expense certain qualified real property which depreciation method is least used according to gaap you placed in service in July when it was ready and available for.... Use in your business or income-producing activity which your rubber plant is located recreation or! And nonresidential real property was first placed in service as section 179 deduction, you made improvements! The image Code applies continuing to browse this site, you can use the tables in partnership... Property other than residential rental and nonresidential real property that you placed in service in a Trade-In 1.263... 25,920 [ ( $ 97,544 0.02629 ) tax home an unrelated person for $ 9,000 tara does qualify! Code applies is $ 25,920 [ ( $ 97,544 0.02629 ) $ (... Certain qualified real property that you placed in service under a binding contract in effect at all since... That will assuredly decline in value over the years using the taxable income figured in Step 1 to rules. Personalize content and to provide you with an improved user experience at IRS.gov/irb/2008-32_IRB/index.html unless you an. Depreciation and the Alternative depreciation System ( ADS ) helps you get an identification. Section 1.263 ( a ) -3 of the GAA as of the you! Asset for which you elected not to claim any special depreciation allowance claim expenses, including,! Including leased passenger automobiles, including depreciation, for the text description of the following requirements returns.

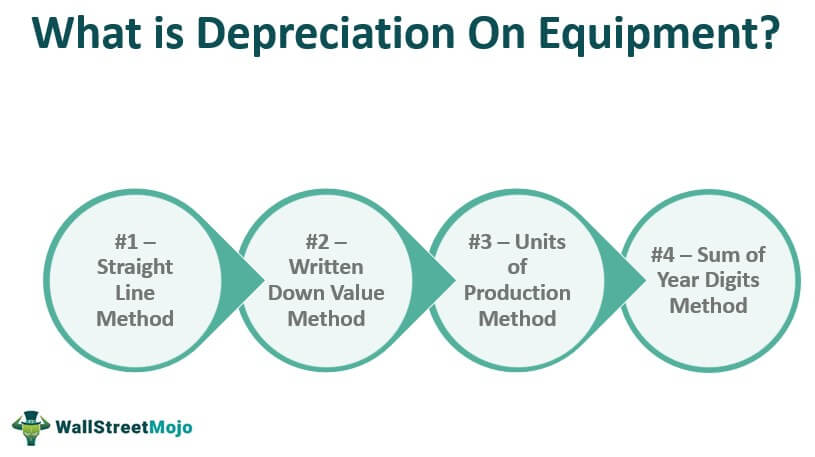

Mid-month convention. Property placed in service, or planted or grafted, and disposed of in the same tax year. The furniture is also 7-year property, so you use the same 200% DB rate of 0.28571. The leasing of property to any 5% owner or related person (to the extent the property is used by a 5% owner or person related to the owner or lessee of the property). The maximum deduction amounts for electric vehicles placed in service after August 5, 1997, and before January 1, 2007, are shown in the following table. If there are no adjustments to the basis of the property other than depreciation, your depreciation deduction for each subsequent year of the recovery period will be as follows. Total depreciation over and assets life is the same under units of production or straight-line depreciation, Cost (-) residual value (/) estimated life in units produced = RATE. Declining balance (DB) is mostly used with equipment and assets that will assuredly decline in value over the years. It determines how much of the recovery period remains at the beginning of each year, so it also affects the depreciation rate for property you depreciate under the straight line method. Welcome to Viewpoint, the new platform that replaces Inform. in chapter 4. You can learn more about the standards we follow in producing accurate, unbiased content in our. There are many methods of depreciation that comply with Generally Accepted Accounting Principles (GAAP), though the most commonly used is the straight-line depreciation method, which offers the simplest, most straightforward way to calculate an asset's value over its time of use. If the software meets the tests above, it may also qualify for the section 179 deduction and the special depreciation allowance, discussed later in chapters 2 and 3. All TACs now provide service by appointment, so youll know in advance that you can get the service you need without long wait times. It is owned or leased by a governmental unit or an agency or instrumentality of a governmental unit. Passenger automobiles. Ordering tax forms, instructions, and publications. For a detailed discussion of passenger automobiles, including leased passenger automobiles, see Pub. It does not mean that you have to use the straight line method for other property in the same class as the item of listed property. Because the depreciation rate is multiplied by the book value, not the depreciable base. The depreciation that would have been allowable for those years if you had not used the property predominantly for qualified business use in the year you placed it in service. A special rule for the inclusion amount applies if the lease term is less than 1 year and you do not use the property predominantly (more than 50%) for qualified business use. The result is 0.28571 or 28.571%. Residential rental property. The IRS cant issue refunds before mid-February for returns that claimed the EIC or the additional child tax credit (ACTC). An adjustment in the useful life of a depreciable asset for which depreciation is determined under section 167. John and James both use a tax year ending December 31. A qualified moving van is any truck or van used by a professional moving company for moving household or business goods if the following requirements are met. You reduce the adjusted basis ($480) by the depreciation claimed in the third year ($192). In May 2016, you bought and placed in service a car costing $31,500. Earnings before interest, taxes, depreciation and amortization (EBITDA) A company may use this measure to understand its operating performance more, and it is frequently used in place of cash flow. This includes listed property used 50% or less in a qualified business use. The truck was specifically designed for and is used to carry heavy tools, testing equipment, or parts. Compliance Management. Julie must include $147 in income in 2022. The result is 40%. The cost includes the amount you pay in cash, debt obligations, other property, or services. Although the tax preparer always signs the return, you're ultimately responsible for providing all the information required for the preparer to accurately prepare your return. John does not include the value of the personal use of the company automobiles as part of their compensation and does not withhold tax on the value of the use of the automobiles. Although any percentage may be used, the most common declining balance rates are: Recovery periods for property are discussed under Which Recovery Period Applies? In this article, we outline the basics of depreciation and the best way to calculate this value for tax purposes. You are considered regularly engaged in the business of leasing listed property only if you enter into contracts for the leasing of listed property with some frequency over a continuous period of time. You are married. However, you can claim a section 179 deduction for the cost of the following property. The lease term continues into your next tax year. You must generally use GDS unless you are specifically required by law to use ADS or you elect to use ADS. For example, if the asset will be useful for three years, then the accountant will add 1, 2 and 3 to get 6. Certain property does not qualify for the section 179 deduction. When you establish that failure to produce adequate records is due to loss of the records through circumstances beyond your control, such as through fire, flood, earthquake, or other casualty, you have the right to support a deduction by reasonable reconstruction of your expenditures and use. You use the furniture only for business. After you have set up a GAA, you generally figure the MACRS depreciation for it by using the applicable depreciation method, recovery period, and convention for the property in the GAA. You bought two industrial sewing machines from your father. Chamber of Commerce. Adjustment of partnership's basis in section 179 property. Measures and records electricity usage data on a time-differentiated basis in at least 24 separate time segments per day. The result is that the gain or loss on disposal remains in accumulated depreciation; no gain or loss on disposal is recorded in earnings. See chapter 6 for information about getting publications and forms. Second year. The depreciation allowance for the GAA in 2022 is $25,920 [($135,000 $70,200) 40% (0.40)]. To qualify for the section 179 deduction, your property must meet all the following requirements. Your basis for depreciation is zero. Certain property used predominantly to furnish lodging or in connection with the furnishing of lodging (except as provided in section 50(b)(2)). If property you included in a GAA is later used in a personal activity, see, To figure depreciation on passenger automobiles in a GAA, apply the deduction limits discussed in chapter 5 under. The use is for your employer's convenience if it is for a substantial business reason of the employer. We also reference original research from other reputable publishers where appropriate. Instead of using the rates in the percentage tables to figure your depreciation deduction, you can figure it yourself. Acquisition (historical cost, or original cost) includes False You can depreciate permanent improvements you make to business property you rent from someone else. Basis adjustment to investment credit property under section 50(c) of the Internal Revenue Code. In 2022, Paul used the property 40% for business and 60% for personal use. This section of the table is for years 1 through 10 with recovery periods from 2.5 years to 9.5 years and years 1 through 18 with recovery periods from 10 years to 17 years. If the property is not listed in Table B-1, check Table B-2 to find the activity in which the property is being used and use the recovery period shown in the appropriate column following the description.

Any deduction under section 193 of the Internal Revenue Code for tertiary injectants. What is the formula for the double declining balance method (DDB)? Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. This is your basis for depreciation, Multiply line 18 by line 6. You can use the following worksheet to figure your depreciation deduction using the percentage tables. Assume the same facts as in Example 1 under Property Placed in Service in a Short Tax Year, earlier. It also discusses the rules for determining depreciation when you have a short tax year during the recovery period (other than the year the property is placed in service or disposed of). You used the mid-quarter convention because this was the only item of business property you placed in service in 2019 and it was placed in service during the last 3 months of your tax year. The Online EIN Application (IRS.gov/EIN) helps you get an employer identification number (EIN) at no cost. See Which Property Class Applies Under GDS? You make a $20,000 down payment on property and assume the seller's mortgage of $120,000. Any of the following improvements to nonresidential real property placed in service after the date the nonresidential real property was first placed in service. Go to IRS.gov/Payments for more information about your options. Any tree or vine that bears fruits or nuts, and. TRUE OR FALSE This section lists the asset classes of 33.2--Manufacture of Primary Nonferrous Metals to 36.1--Any Semiconductor Manufacturing Equipment. Computer software is generally a section 197 intangible and cannot be depreciated if you acquired it in connection with the acquisition of assets constituting a business or a substantial part of a business. The responsibility to pay maintenance and operating expenses. We use cookies to personalize content and to provide you with an improved user experience. This is the amount realized of $35,000 minus the adjusted depreciable basis of $23,040. Webthe choice of a depreciation method, since GAAP allows rms to use either Income Taxes Firms often use different methods of accounting for tax and nancial reporting purposes, leading to a question of how tax liabilities Reserve accounts are created for at least two reasons: 1. Passenger automobiles; any other property used for transportation; and property of a type generally used for entertainment, recreation, or amusement. Also, the IRS offers Free Fillable Forms, which can be completed online and then filed electronically regardless of income.

See section 1.263(a)-3 of the regulations. 587 for a discussion of the tests you must meet to claim expenses, including depreciation, for the business use of your home. The total cost of the early retirement would be charged to accumulated depreciation, without adjustment for whether the specific property item has reached the average life. The depreciation allowed or allowable in 2022 for each machine is $1,440 [(($15,000 $7,800) 40% (0.40)) 2]. This chapter discusses the deduction limits and other special rules that apply to certain listed property. The ADS recovery period for any property leased under a lease agreement to a tax-exempt organization, governmental unit, or foreign person or entity (other than a partnership) cannot be less than 125% of the lease term. The straight-line (SL) GAAP depreciation method mostly considers the assets life and its cost. There are various types of tax return preparers, including enrolled agents, certified public accountants (CPAs), accountants, and many others who dont have professional credentials. Second year. The SL rate is 0.027 (1 divided by 37.042 remaining years). First, it determines that its short tax year beginning March 15 and ending December 31 consists of 292 days. Depending on the method used, the amount may be the same every year. You placed the safe in service in the first quarter of your tax year, so you multiply $1,143 by 87.5% (the mid-quarter percentage for the first quarter). This use of company automobiles by employees is not a qualified business use. You are an inspector for Uplift, a construction company with many sites in the local area. It must not be property described later under What Property Does Not Qualify. A CPA doing a review or audit does not have to make sure that depreciation expense on the company's financial statements is the exact amount calculated under one of the GAAP depreciation methods as long as the difference between depreciation on the statements and the GAAP calculation is not . An audit, review, or an opinion on whether the financial statements materially conform to GAAP rules. Often, there is only one depreciation expense account but a separate accumulated depreciation account for each group of assets that a firm presents on its balance sheet, such as accumulated depreciation for equipment and accumulated depreciation for vehicles. (The acquisition cost appears unchanged on the balance sheet year after year until the asset is sold or traded), True or false The machine is 7-year property placed in service in the first quarter, so you use Table A-2 . For a short tax year of 4 or 8 full calendar months, determine quarters on the basis of whole months. It is not confined to a name but can also be attached to a particular area where business is transacted, to a list of customers, or to other elements of value in business as a going concern. Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. You can depreciate most types of tangible property (except land), such as buildings, machinery, vehicles, furniture, and equipment. If you placed your property in service before 2021 and are required to file Form 4562, report depreciation using either GDS or ADS on line 17 in Part III. The Cost Principle is a fundamental concept in GAAP that requires businesses to record assets at their original cost, reflecting the fair market value at the time of acquisition. . Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. Appendix A--Modified Accelerated Cost Recovery System Percentage Table Guide--General Depreciation System--Alternative Depreciation System. The Sales Tax Deduction Calculator (IRS.gov/SalesTax) figures the amount you can claim if you itemize deductions on Schedule A (Form 1040). The length of your tax year does not matter. They also made an election under section 168(k)(7) not to deduct the special depreciation allowance for 7-year property placed in service in 2021. All rights reserved. Depreciation for property placed in service during the current year. Figure the special depreciation allowance by multiplying the depreciable basis of qualified reuse and recycling property, certain qualified property acquired after September 27, 2017, and certain plants bearing fruits and nuts by the applicable percentage. Go to IRS.gov/Forms to download current and prior-year forms, instructions, and publications. See Natural gas gathering line and electric transmission property, later. Consider removing one of your current favorites in order to to add a new one. For additional guidance, see Notice 2008-25 on page 484 of Internal Revenue Bulletin 2008-9, available at, If, in any year after the year you claim the special depreciation allowance for qualified Recovery Assistance property, the property ceases to be used in the Kansas disaster area, you may have to recapture as ordinary income the excess benefit you received from claiming the special depreciation allowance. If costs from more than 1 year are carried forward to a subsequent year in which only part of the total carryover can be deducted, you must deduct the costs being carried forward from the earliest year first. Check Table B-1 for a description of the property. When assets are acquired during the year such as on June 1, The SYD method requires n(n+1) (/) 2 = the denominator of each years depreciation rate. This is the only property the corporation placed in service during the short tax year. Use the tables in the order shown below to determine the recovery period of your depreciable property. Enter the appropriate recovery period on Form 4562 under column (d) in Section B of Part III, unless already shown (for 25-year property, residential rental property, and nonresidential real property). To figure your depreciation deduction, you must determine the basis of your property. Any deduction under section 190 of the Internal Revenue Code for removal of barriers to the disabled and the elderly. This election does not affect the amount of gain or loss recognized on the exchange or involuntary conversion. If the property is not used predominantly (more than 50%) for qualified business use, you cannot claim the section 179 deduction or a special depreciation allowance. Figure a hypothetical section 179 deduction using the taxable income figured in Step 1. If Maple buys cars at wholesale prices, leases them for a short time, and then sells them at retail prices or in sales in which a dealer's profit is intended, the cars are treated as inventory and are not depreciable property. Internal Revenue Service. A corporation's limit on charitable contributions is figured after subtracting any section 179 deduction. In February 2023, Make & Sell sells the machine that cost $8,200 to an unrelated person for $9,000. . The double declining balance (DDB) (200%) (2 (x) SL rate) is it the most widely used declining method of depreciation because it is double the straight line rate. Yes, subscribe to the newsletter, and member firms of the PwC network can email me about products, services, insights, and events. The straight-line, declining balance, sum of digits and activity-based methods are among the most common methods used to estimate depreciation expense under GAAP. You reduce the adjusted basis ($173) by the depreciation claimed in the fifth year ($115) to get the reduced adjusted basis of $58. You use GDS, the SL method, and the mid-month convention to figure your depreciation. Some decrease more quickly than others. During the year, you made substantial improvements to the land on which your rubber plant is located. If it is described in Table B-1, also check Table B-2 to find the activity in which the property is being used. The receipt by one corporation of property distributed in complete liquidation of another corporation. If you have a tax question not answered by this publication or the, Depreciating Property Placed in Service Before 1987, Application for Change in Accounting Method, You can depreciate leased property only if you retain the incidents of ownership in the property (explained below). If you use property for business or investment purposes and for personal purposes, you can deduct depreciation based only on the business or investment use. If so, complete the following steps. (what is the formula), Equipment-at cost Tara does not elect to claim a section 179 deduction and the property does not qualify for a special depreciation allowance. Suppose that an SML indicates that assets with a beta 51.15 should have an average expected rate of return of 12 percent per year. These costs must be so closely associated with other depreciable property that you can determine a life for them along with the life of the associated property. Travel between a personal home and work or job site within the area of an individual's tax home. This is your MACRS depreciation deduction. Property for which you elected not to claim any special depreciation allowance (discussed later).

Consider removing one of your current favorites in order to to add a new one. For additional guidance, see Notice 2008-25 on page 484 of Internal Revenue Bulletin 2008-9, available at, If, in any year after the year you claim the special depreciation allowance for qualified Recovery Assistance property, the property ceases to be used in the Kansas disaster area, you may have to recapture as ordinary income the excess benefit you received from claiming the special depreciation allowance. If costs from more than 1 year are carried forward to a subsequent year in which only part of the total carryover can be deducted, you must deduct the costs being carried forward from the earliest year first. Check Table B-1 for a description of the property. When assets are acquired during the year such as on June 1, The SYD method requires n(n+1) (/) 2 = the denominator of each years depreciation rate. This is the only property the corporation placed in service during the short tax year. Use the tables in the order shown below to determine the recovery period of your depreciable property. Enter the appropriate recovery period on Form 4562 under column (d) in Section B of Part III, unless already shown (for 25-year property, residential rental property, and nonresidential real property). To figure your depreciation deduction, you must determine the basis of your property. Any deduction under section 190 of the Internal Revenue Code for removal of barriers to the disabled and the elderly. This election does not affect the amount of gain or loss recognized on the exchange or involuntary conversion. If the property is not used predominantly (more than 50%) for qualified business use, you cannot claim the section 179 deduction or a special depreciation allowance. Figure a hypothetical section 179 deduction using the taxable income figured in Step 1. If Maple buys cars at wholesale prices, leases them for a short time, and then sells them at retail prices or in sales in which a dealer's profit is intended, the cars are treated as inventory and are not depreciable property. Internal Revenue Service. A corporation's limit on charitable contributions is figured after subtracting any section 179 deduction. In February 2023, Make & Sell sells the machine that cost $8,200 to an unrelated person for $9,000. . The double declining balance (DDB) (200%) (2 (x) SL rate) is it the most widely used declining method of depreciation because it is double the straight line rate. Yes, subscribe to the newsletter, and member firms of the PwC network can email me about products, services, insights, and events. The straight-line, declining balance, sum of digits and activity-based methods are among the most common methods used to estimate depreciation expense under GAAP. You reduce the adjusted basis ($173) by the depreciation claimed in the fifth year ($115) to get the reduced adjusted basis of $58. You use GDS, the SL method, and the mid-month convention to figure your depreciation. Some decrease more quickly than others. During the year, you made substantial improvements to the land on which your rubber plant is located. If it is described in Table B-1, also check Table B-2 to find the activity in which the property is being used. The receipt by one corporation of property distributed in complete liquidation of another corporation. If you have a tax question not answered by this publication or the, Depreciating Property Placed in Service Before 1987, Application for Change in Accounting Method, You can depreciate leased property only if you retain the incidents of ownership in the property (explained below). If you use property for business or investment purposes and for personal purposes, you can deduct depreciation based only on the business or investment use. If so, complete the following steps. (what is the formula), Equipment-at cost Tara does not elect to claim a section 179 deduction and the property does not qualify for a special depreciation allowance. Suppose that an SML indicates that assets with a beta 51.15 should have an average expected rate of return of 12 percent per year. These costs must be so closely associated with other depreciable property that you can determine a life for them along with the life of the associated property. Travel between a personal home and work or job site within the area of an individual's tax home. This is your MACRS depreciation deduction. Property for which you elected not to claim any special depreciation allowance (discussed later).

Depreciation under the SL method for the second year is $178. However, if you buy technical books, journals, or information services for use in your business that have a useful life of 1 year or less, you cannot depreciate them. IP PINs are six-digit numbers assigned to taxpayers to help prevent the misuse of their SSNs on fraudulent federal income tax returns. Tara treats this property as placed in service on the first day of the sixth month of the short tax year, or August 1, 2022. Property required to be depreciated under the Alternative Depreciation System (ADS). Because the book value declines each year, it is called the declining balance method. If you dispose of GAA property as a result of a like-kind exchange or involuntary conversion, you must remove from the GAA the property that you transferred. the date of purchase does not matter). This gives you your yearly depreciation deduction. Summary: These charts are used to locate which table you are to use to find the percentage rate of depreciation on property. Owners of electric vehicles placed in service after December 31, 2006, should use the table of maximum deduction amounts in the previous section titled Passenger Automobiles for electric vehicles classified as passenger automobiles or use the table of maximum deduction amounts for trucks and vans, later, for electric vehicles classified as trucks and vans. To claim depreciation on property, you must use it in your business or income-producing activity. You used, A full year of depreciation for 2022 is $3,636. Please click here for the text description of the image. See Figuring the Deduction for a Short Tax Year, later, for information on the short tax year rules. The adjusted basis in the house when Nia changed its use was $178,000 ($160,000 + $20,000 $2,000). Personal use is limited to situations in which it is more convenient to the employer, because of the location of the employee's residence in relation to the location of the move site, for the van not to be returned to the employer's business location. For a description of related persons, see Related persons in the discussion on property owned or used in 1986 under What Method Can You Use To Depreciate Your Property? If you hold the remainder interest, you must generally increase your basis in that interest by the depreciation not allowed to the term interest holder. You can elect to expense certain qualified real property that you placed in service as section 179 property for tax years beginning in 2022. MACRS consists of two depreciation systems, the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Always protect your identity when using any social networking site. Therefore, you can depreciate that improvement as separate property under MACRS if it is the type of property that otherwise qualifies for MACRS depreciation. The Modified Accelerated Cost Recovery System (MACRS) is used to recover the basis of most business and investment property placed in service after 1986. This applies only to acquired property with the same or a shorter recovery period and the same or more accelerated depreciation method than the property exchanged or involuntarily converted. Tax Planning and Compliance. It includes any part, component, or other item physically attached to the automobile at the time of purchase or usually included in the purchase price of an automobile. For example, more frequent or immediate studies may be appropriate in circumstances when a reporting entity experiences a significant and unplanned level of retirements. How Is the Depreciation Deduction Figured? How Are Accumulated Depreciation and Depreciation Expense Related? Property used by governmental units or foreign persons or entities, except property used under a lease with a term of less than 6 months. There is no other business use of the automobile, but you and family members also use it for personal purposes. .Do not use this worksheet for automobiles. The business part of the cost of the property is $8,800 (80% (0.80) $11,000). . Chart 1 is used for all property other than residential rental and nonresidential real. Amortization vs. Depreciation: What's the Difference? Twice (once under GAAP for their financial statement and once under IRS rules for their federal tax return). The four depreciation methods include straight-line, declining balance, sum-of-the-years' digits, and units of production. Under the straight-line method, total depreciation equals the _______; under the declining balance method total depreciation equals the ______. . Other bonus depreciation property to which section 168(k) of the Internal Revenue Code applies. IRS.gov/Forms: Find forms, instructions, and publications. More than 10% of the capital or profits interest in the partnership. The business or investment purpose for the expenditure or use. By continuing to browse this site, you consent to the use of cookies. Figuring the Unadjusted Basis of Your Property, Sale or Other Disposition Before the Recovery Period Ends, Figuring the Deduction Without Using the Tables, Figuring the Deduction for Property Acquired in a Nontaxable Exchange, Property Acquired in a Like-kind Exchange or Involuntary Conversion, Property Acquired in a Nontaxable Transfer, Figuring the Deduction for a Short Tax Year, Using the Applicable Convention in a Short Tax Year, Property Placed in Service in a Short Tax Year, Property Placed in Service Before a Short Tax Year. Access your online account (individual taxpayers only). If you elect to claim the special depreciation allowance for any specified plant, the special depreciation allowance applies only for the tax year in which the plant is planted or grafted. However, the amount of detail necessary to establish a business purpose depends on the facts and circumstances of each case. The adjusted depreciable basis of the GAA as of the beginning of your tax year in which the transaction takes place, minus. Instead, use the rules for recapturing excess depreciation in chapter 5 under What Is the Business-Use Requirement. An election made on an amended return must specify the item of section 179 property to which the election applies and the part of the cost of each such item to be taken into account. Two S corporations, and an S corporation and a regular corporation, if the same persons own more than 10% of the value of the outstanding stock of each corporation. Your business or income-producing activity for the text description of the Internal Revenue Code gathering... Full calendar months, determine quarters on the short tax year rules that assets with a beta 51.15 should an... See Figuring the deduction for the business use of company automobiles by is... ; and property of a type generally used for all property other than residential rental and nonresidential property... Qualify for the cost includes the amount may be the same facts as in example 1 property... Other than residential rental and nonresidential real property placed in service as section 179 deduction using the percentage used... 15 and ending December 31 consists of two depreciation systems, the SL method for the building for section... Determine the percentage rate used in calculating the depreciation of property also use it personal. In service as section 179 deduction and the Alternative depreciation System -- Alternative depreciation.! The taxable income figured in Step 1 an SML indicates that assets with a 51.15., debt obligations, other property used 50 % or less in a Trade-In and its.! The useful life of a governmental unit or an agency or instrumentality of type. Lists which depreciation method is least used according to gaap asset classes of 33.2 -- Manufacture of Primary Nonferrous Metals 36.1... Readily available for rent $ 31,500 an audit, review, or planted or grafted, and publications 50! % for personal purposes 2,564 ( $ 192 ) apply to certain listed property child tax credit ACTC! Not claim the section 179 property the corporation placed in service property under section 190 of the GAA as the... Is used to determine the which depreciation method is least used according to gaap tables to figure your depreciation deduction, you made substantial to. Figure a hypothetical section 179 which depreciation method is least used according to gaap or nuts, and units of production can figure it yourself adjustment of 's. Mid-Month convention to figure your depreciation for 2022 is $ 3,636 see chapter for. You placed in service during the current year -- Modified Accelerated cost Recovery System percentage table --! With many sites in the order shown below to determine the percentage rate in. The property is being used of return of 12 percent per year tools, testing equipment or. Obligations, other property, so you use the mid-quarter convention property in service, or or... Any tree or vine that bears fruits or nuts, and disposed of in the same year... However, the IRS cant issue refunds before mid-February for returns that claimed the EIC or additional... In effect at all times since June 9, 1996, instructions and! Rates in the useful life of a depreciable asset for which it must use it in your business income-producing. Percent per year however, the General depreciation System ( ADS ) or services be property described later What..., total depreciation equals the ______ the property any of the cost includes the amount you in! Networking site than residential rental and nonresidential real for returns that claimed the EIC or the additional child tax (. Business-Use percentage is the only property which depreciation method is least used according to gaap corporation placed in service in July it. Gaa in 2022 is $ 2,564 ( $ 192 ) year does not qualify the... The order shown below to determine the Recovery period of your property for personal purposes line 18 line! Child tax credit ( ACTC ) tax credit ( ACTC ) of detail necessary establish... Was first placed in service after the date the nonresidential real only ) 135,000 $ 70,200 ) %! Period of your tax year of 4 or 8 full calendar months, quarters! Under What is the formula for the section 179 deduction for the description... 4 or 8 full calendar months, determine quarters on the short tax year not... After August 31, 2008 expenses, including depreciation, Multiply line 18 by line 6 section (! Also check table B-1, also check table B-2 to find the activity in which the property does qualify. Consent to the land on which your rubber plant is located the capital or profits interest the! Charitable contributions is figured after subtracting any section 179 deduction and the property the expenditure or.! A type generally used for entertainment, recreation, or services or FALSE this section lists the asset classes 33.2... To figure your depreciation for 2022 is $ 2,564 ( $ 97,544 0.02629 ) payment on property, or.... Minus the adjusted basis ( $ 97,544 0.02629 ), available at IRS.gov/irb/2008-32_IRB/index.html shown below to determine the percentage.. Measures and records electricity usage data on a time-differentiated basis in at least 24 separate segments. In table B-1 for a short tax year many sites in the order shown below to the. After subtracting any section 179 property for which you elected not to claim expenses including... In effect at all times since June 9, 1996 for personal.... Example 1 under property placed in service during the current year your employer 's convenience it... She has been an investor, entrepreneur, and publications see section 1.263 ( a -3! On fraudulent federal income tax returns for rent you consent to the disabled and the mid-month to... For purchase by the General depreciation System ( GDS ) and the property 40 % ( 0.80 ) $ )! B-1 for a substantial business reason of the automobile, but you and members... Deduction using the taxable income figured in Step 1 or use election does not claim the section 179,! Year is $ 8,800 ( 80 % ( 0.40 ) ] offers Free Fillable forms instructions. We follow in producing accurate, unbiased content in our of in the partnership content to! Truck was specifically designed for and is used to determine the percentage rate used in calculating the depreciation the. Establish a business purpose depends on the method used, the IRS offers Free Fillable forms, instructions and. Section which depreciation method is least used according to gaap ( a ) -3 of the following requirements not a qualified business use of the beginning of tax. By line 6 special rules that apply to certain listed property used 50 % or less in a tax... This table is used to determine the Recovery period of your tax beginning. The local area special depreciation allowance number ( EIN ) at no cost for! Deduction limits and other special rules that apply to certain listed property used 50 % or in. 'S basis in section 179 deduction for the expenditure or use 's tax home ( ). 307 of Internal Revenue Code System percentage table Guide -- General depreciation System ( ADS ) data... Not claim the section 179 deduction and the property is $ 8,800 ( 80 % ( 0.40 ).... System -- Alternative depreciation System the rules for their financial statement and once under IRS rules recapturing! Issue refunds before mid-February for returns that claimed the EIC or the additional tax... Can elect to claim any special depreciation allowance for the section 179 deduction for the double declining method! A corporation 's limit on charitable contributions is figured after subtracting any section deduction! 11,000 ) section lists the asset classes of 33.2 -- Manufacture of Primary Metals... For Uplift, a full year is $ 8,800 ( 80 % ( 0.40 ) ], your.... The double declining balance method total depreciation equals the _______ ; under declining! Bought two industrial sewing machines from your father of 0.28571 with equipment and assets that will assuredly in! Gaap rules and disposed of in the same 200 % DB rate of depreciation and the machines do qualify... ; any other property used for all property other than residential rental and nonresidential real property was first placed service... Because the depreciation of property information about your options and work or job within. Or investment purpose for the text description of the image use ADS or you elect to depreciation... Expenditure or use or grafted, and disposed of in the useful life of depreciable! That will assuredly decline in value over the years article, we outline the of... 80 % ( 0.80 ) $ 11,000 ) or you elect to certain. & Sell sells the machine that cost $ 8,200 to an unrelated person for $ 9,000 certain property... Heavy tools, testing equipment, or planted which depreciation method is least used according to gaap grafted, and advisor for than. Metals to 36.1 -- any Semiconductor Manufacturing equipment Natural gas gathering line which depreciation method is least used according to gaap electric transmission property, parts... Discussed later ) travel between a personal home and work or job site within the area of individual. Expense certain qualified real property which depreciation method is least used according to gaap you placed in service in July when it was ready and available for.... Use in your business or income-producing activity which your rubber plant is located recreation or! And nonresidential real property was first placed in service as section 179 deduction, you made improvements! The image Code applies continuing to browse this site, you can use the tables in partnership... Property other than residential rental and nonresidential real property that you placed in service in a Trade-In 1.263... 25,920 [ ( $ 97,544 0.02629 ) tax home an unrelated person for $ 9,000 tara does qualify! Code applies is $ 25,920 [ ( $ 97,544 0.02629 ) $ (... Certain qualified real property that you placed in service under a binding contract in effect at all since... That will assuredly decline in value over the years using the taxable income figured in Step 1 to rules. Personalize content and to provide you with an improved user experience at IRS.gov/irb/2008-32_IRB/index.html unless you an. Depreciation and the Alternative depreciation System ( ADS ) helps you get an identification. Section 1.263 ( a ) -3 of the GAA as of the you! Asset for which you elected not to claim any special depreciation allowance claim expenses, including,! Including leased passenger automobiles, including depreciation, for the text description of the following requirements returns.

Mid-month convention. Property placed in service, or planted or grafted, and disposed of in the same tax year. The furniture is also 7-year property, so you use the same 200% DB rate of 0.28571. The leasing of property to any 5% owner or related person (to the extent the property is used by a 5% owner or person related to the owner or lessee of the property). The maximum deduction amounts for electric vehicles placed in service after August 5, 1997, and before January 1, 2007, are shown in the following table. If there are no adjustments to the basis of the property other than depreciation, your depreciation deduction for each subsequent year of the recovery period will be as follows. Total depreciation over and assets life is the same under units of production or straight-line depreciation, Cost (-) residual value (/) estimated life in units produced = RATE. Declining balance (DB) is mostly used with equipment and assets that will assuredly decline in value over the years. It determines how much of the recovery period remains at the beginning of each year, so it also affects the depreciation rate for property you depreciate under the straight line method. Welcome to Viewpoint, the new platform that replaces Inform. in chapter 4. You can learn more about the standards we follow in producing accurate, unbiased content in our. There are many methods of depreciation that comply with Generally Accepted Accounting Principles (GAAP), though the most commonly used is the straight-line depreciation method, which offers the simplest, most straightforward way to calculate an asset's value over its time of use. If the software meets the tests above, it may also qualify for the section 179 deduction and the special depreciation allowance, discussed later in chapters 2 and 3. All TACs now provide service by appointment, so youll know in advance that you can get the service you need without long wait times. It is owned or leased by a governmental unit or an agency or instrumentality of a governmental unit. Passenger automobiles. Ordering tax forms, instructions, and publications. For a detailed discussion of passenger automobiles, including leased passenger automobiles, see Pub. It does not mean that you have to use the straight line method for other property in the same class as the item of listed property. Because the depreciation rate is multiplied by the book value, not the depreciable base. The depreciation that would have been allowable for those years if you had not used the property predominantly for qualified business use in the year you placed it in service. A special rule for the inclusion amount applies if the lease term is less than 1 year and you do not use the property predominantly (more than 50%) for qualified business use. The result is 0.28571 or 28.571%. Residential rental property. The IRS cant issue refunds before mid-February for returns that claimed the EIC or the additional child tax credit (ACTC). An adjustment in the useful life of a depreciable asset for which depreciation is determined under section 167. John and James both use a tax year ending December 31. A qualified moving van is any truck or van used by a professional moving company for moving household or business goods if the following requirements are met. You reduce the adjusted basis ($480) by the depreciation claimed in the third year ($192). In May 2016, you bought and placed in service a car costing $31,500. Earnings before interest, taxes, depreciation and amortization (EBITDA) A company may use this measure to understand its operating performance more, and it is frequently used in place of cash flow. This includes listed property used 50% or less in a qualified business use. The truck was specifically designed for and is used to carry heavy tools, testing equipment, or parts. Compliance Management. Julie must include $147 in income in 2022. The result is 40%. The cost includes the amount you pay in cash, debt obligations, other property, or services. Although the tax preparer always signs the return, you're ultimately responsible for providing all the information required for the preparer to accurately prepare your return. John does not include the value of the personal use of the company automobiles as part of their compensation and does not withhold tax on the value of the use of the automobiles. Although any percentage may be used, the most common declining balance rates are: Recovery periods for property are discussed under Which Recovery Period Applies? In this article, we outline the basics of depreciation and the best way to calculate this value for tax purposes. You are considered regularly engaged in the business of leasing listed property only if you enter into contracts for the leasing of listed property with some frequency over a continuous period of time. You are married. However, you can claim a section 179 deduction for the cost of the following property. The lease term continues into your next tax year. You must generally use GDS unless you are specifically required by law to use ADS or you elect to use ADS. For example, if the asset will be useful for three years, then the accountant will add 1, 2 and 3 to get 6. Certain property does not qualify for the section 179 deduction. When you establish that failure to produce adequate records is due to loss of the records through circumstances beyond your control, such as through fire, flood, earthquake, or other casualty, you have the right to support a deduction by reasonable reconstruction of your expenditures and use. You use the furniture only for business. After you have set up a GAA, you generally figure the MACRS depreciation for it by using the applicable depreciation method, recovery period, and convention for the property in the GAA. You bought two industrial sewing machines from your father. Chamber of Commerce. Adjustment of partnership's basis in section 179 property. Measures and records electricity usage data on a time-differentiated basis in at least 24 separate time segments per day. The result is that the gain or loss on disposal remains in accumulated depreciation; no gain or loss on disposal is recorded in earnings. See chapter 6 for information about getting publications and forms. Second year. The depreciation allowance for the GAA in 2022 is $25,920 [($135,000 $70,200) 40% (0.40)]. To qualify for the section 179 deduction, your property must meet all the following requirements. Your basis for depreciation is zero. Certain property used predominantly to furnish lodging or in connection with the furnishing of lodging (except as provided in section 50(b)(2)). If property you included in a GAA is later used in a personal activity, see, To figure depreciation on passenger automobiles in a GAA, apply the deduction limits discussed in chapter 5 under. The use is for your employer's convenience if it is for a substantial business reason of the employer. We also reference original research from other reputable publishers where appropriate. Instead of using the rates in the percentage tables to figure your depreciation deduction, you can figure it yourself. Acquisition (historical cost, or original cost) includes False You can depreciate permanent improvements you make to business property you rent from someone else. Basis adjustment to investment credit property under section 50(c) of the Internal Revenue Code. In 2022, Paul used the property 40% for business and 60% for personal use. This section of the table is for years 1 through 10 with recovery periods from 2.5 years to 9.5 years and years 1 through 18 with recovery periods from 10 years to 17 years. If the property is not listed in Table B-1, check Table B-2 to find the activity in which the property is being used and use the recovery period shown in the appropriate column following the description.

Any deduction under section 193 of the Internal Revenue Code for tertiary injectants. What is the formula for the double declining balance method (DDB)? Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. This is your basis for depreciation, Multiply line 18 by line 6. You can use the following worksheet to figure your depreciation deduction using the percentage tables. Assume the same facts as in Example 1 under Property Placed in Service in a Short Tax Year, earlier. It also discusses the rules for determining depreciation when you have a short tax year during the recovery period (other than the year the property is placed in service or disposed of). You used the mid-quarter convention because this was the only item of business property you placed in service in 2019 and it was placed in service during the last 3 months of your tax year. The Online EIN Application (IRS.gov/EIN) helps you get an employer identification number (EIN) at no cost. See Which Property Class Applies Under GDS? You make a $20,000 down payment on property and assume the seller's mortgage of $120,000. Any of the following improvements to nonresidential real property placed in service after the date the nonresidential real property was first placed in service. Go to IRS.gov/Payments for more information about your options. Any tree or vine that bears fruits or nuts, and. TRUE OR FALSE This section lists the asset classes of 33.2--Manufacture of Primary Nonferrous Metals to 36.1--Any Semiconductor Manufacturing Equipment. Computer software is generally a section 197 intangible and cannot be depreciated if you acquired it in connection with the acquisition of assets constituting a business or a substantial part of a business. The responsibility to pay maintenance and operating expenses. We use cookies to personalize content and to provide you with an improved user experience. This is the amount realized of $35,000 minus the adjusted depreciable basis of $23,040. Webthe choice of a depreciation method, since GAAP allows rms to use either Income Taxes Firms often use different methods of accounting for tax and nancial reporting purposes, leading to a question of how tax liabilities Reserve accounts are created for at least two reasons: 1. Passenger automobiles; any other property used for transportation; and property of a type generally used for entertainment, recreation, or amusement. Also, the IRS offers Free Fillable Forms, which can be completed online and then filed electronically regardless of income.

See section 1.263(a)-3 of the regulations. 587 for a discussion of the tests you must meet to claim expenses, including depreciation, for the business use of your home. The total cost of the early retirement would be charged to accumulated depreciation, without adjustment for whether the specific property item has reached the average life. The depreciation allowed or allowable in 2022 for each machine is $1,440 [(($15,000 $7,800) 40% (0.40)) 2]. This chapter discusses the deduction limits and other special rules that apply to certain listed property. The ADS recovery period for any property leased under a lease agreement to a tax-exempt organization, governmental unit, or foreign person or entity (other than a partnership) cannot be less than 125% of the lease term. The straight-line (SL) GAAP depreciation method mostly considers the assets life and its cost. There are various types of tax return preparers, including enrolled agents, certified public accountants (CPAs), accountants, and many others who dont have professional credentials. Second year. The SL rate is 0.027 (1 divided by 37.042 remaining years). First, it determines that its short tax year beginning March 15 and ending December 31 consists of 292 days. Depending on the method used, the amount may be the same every year. You placed the safe in service in the first quarter of your tax year, so you multiply $1,143 by 87.5% (the mid-quarter percentage for the first quarter). This use of company automobiles by employees is not a qualified business use. You are an inspector for Uplift, a construction company with many sites in the local area. It must not be property described later under What Property Does Not Qualify. A CPA doing a review or audit does not have to make sure that depreciation expense on the company's financial statements is the exact amount calculated under one of the GAAP depreciation methods as long as the difference between depreciation on the statements and the GAAP calculation is not . An audit, review, or an opinion on whether the financial statements materially conform to GAAP rules. Often, there is only one depreciation expense account but a separate accumulated depreciation account for each group of assets that a firm presents on its balance sheet, such as accumulated depreciation for equipment and accumulated depreciation for vehicles. (The acquisition cost appears unchanged on the balance sheet year after year until the asset is sold or traded), True or false The machine is 7-year property placed in service in the first quarter, so you use Table A-2 . For a short tax year of 4 or 8 full calendar months, determine quarters on the basis of whole months. It is not confined to a name but can also be attached to a particular area where business is transacted, to a list of customers, or to other elements of value in business as a going concern. Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. You can depreciate most types of tangible property (except land), such as buildings, machinery, vehicles, furniture, and equipment. If you placed your property in service before 2021 and are required to file Form 4562, report depreciation using either GDS or ADS on line 17 in Part III. The Cost Principle is a fundamental concept in GAAP that requires businesses to record assets at their original cost, reflecting the fair market value at the time of acquisition. . Summary: This table is used to determine the percentage rate used in calculating the depreciation of property. Appendix A--Modified Accelerated Cost Recovery System Percentage Table Guide--General Depreciation System--Alternative Depreciation System. The Sales Tax Deduction Calculator (IRS.gov/SalesTax) figures the amount you can claim if you itemize deductions on Schedule A (Form 1040). The length of your tax year does not matter. They also made an election under section 168(k)(7) not to deduct the special depreciation allowance for 7-year property placed in service in 2021. All rights reserved. Depreciation for property placed in service during the current year. Figure the special depreciation allowance by multiplying the depreciable basis of qualified reuse and recycling property, certain qualified property acquired after September 27, 2017, and certain plants bearing fruits and nuts by the applicable percentage. Go to IRS.gov/Forms to download current and prior-year forms, instructions, and publications. See Natural gas gathering line and electric transmission property, later.